Understanding Insurance Risk Management Regulatory Compliance

The insurance industry, by its very nature, deals with risk. Therefore, robust risk management practices are not just best practices, but crucial for the stability of individual insurance companies and the financial system as a whole. Regulatory compliance standards provide a framework for insurers to identify, assess, manage, and monitor various risks. These standards are designed to protect policyholders, maintain solvency, and ensure fair market practices. This article delves into the key aspects of insurance risk management regulatory compliance standards, exploring their importance and the challenges they present.

The Importance of Regulatory Compliance in Insurance

Compliance with insurance risk management regulations is paramount for several reasons:

- Protecting Policyholders: Regulations ensure that insurers have adequate capital reserves to meet their obligations to policyholders, even in adverse circumstances. This safeguards policyholders' financial security and provides confidence in the insurance market.

- Maintaining Solvency: Regulatory standards help prevent insurer insolvency by requiring companies to maintain sufficient capital and manage their assets and liabilities prudently. A solvent insurance industry is essential for economic stability.

- Ensuring Fair Market Practices: Regulations promote fair competition and prevent unfair or deceptive practices that could harm consumers. This includes transparency in pricing, accurate policy information, and fair claims handling.

- Promoting Financial Stability: The insurance industry plays a significant role in the financial system. Effective risk management and regulatory oversight contribute to the overall stability of the financial system by mitigating systemic risks.

- Enhancing Public Trust: Compliance with regulations builds trust in the insurance industry, encouraging individuals and businesses to purchase insurance coverage and protect themselves against potential losses.

Key Regulatory Compliance Standards in Insurance Risk Management

Several key regulatory compliance standards govern insurance risk management. These standards vary by jurisdiction but generally address the following areas:

Capital Adequacy

Capital adequacy requirements are a cornerstone of insurance regulation. These requirements specify the minimum amount of capital insurers must hold relative to their risk exposures. The goal is to ensure that insurers have sufficient resources to absorb unexpected losses and continue operating even in challenging economic conditions.

Capital adequacy is often assessed using risk-based capital (RBC) frameworks, which consider the specific risks faced by each insurer. These frameworks typically require insurers to hold more capital for riskier activities, such as investing in volatile assets or writing policies with high potential losses.

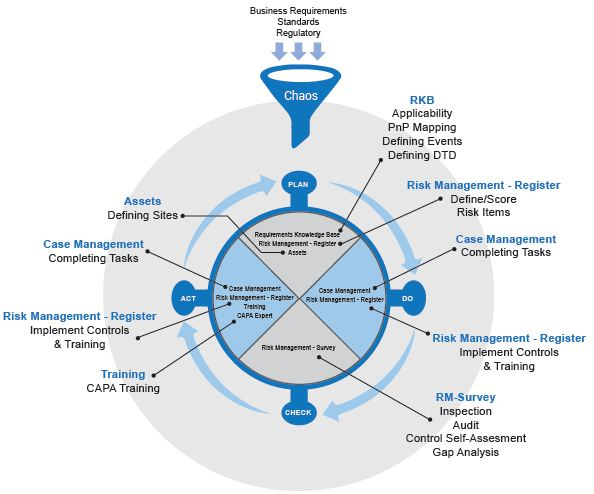

Enterprise Risk Management (ERM)

ERM is a comprehensive approach to risk management that encompasses all aspects of an insurer's operations. Regulatory standards often require insurers to implement ERM frameworks that identify, assess, manage, and monitor all material risks. This includes risks related to underwriting, investments, operations, and reputation.

An effective ERM framework should include a clear risk appetite statement, well-defined risk governance structures, and robust risk reporting processes. It should also be integrated into the insurer's strategic planning and decision-making processes.

Actuarial Standards

Actuarial standards play a critical role in insurance risk management by ensuring that insurers accurately assess and price risks. Actuaries use statistical models and actuarial principles to estimate future claims costs, calculate premiums, and determine appropriate reserves.

Regulatory standards often require insurers to use qualified actuaries to perform these functions and to adhere to established actuarial standards of practice. This helps ensure that insurers are adequately prepared to meet their future obligations.

Investment Regulations

Investment regulations govern how insurers invest their assets. These regulations are designed to protect policyholders by limiting the types of investments insurers can make and by requiring them to maintain a diversified portfolio. The goal is to minimize the risk of investment losses that could jeopardize the insurer's solvency.

Investment regulations often specify limits on investments in particular asset classes, such as equities, real estate, and high-yield bonds. They may also require insurers to hold a certain percentage of their assets in liquid investments that can be easily converted to cash.

Data Security and Privacy Regulations

In today's digital age, data security and privacy are critical concerns for insurers. Insurers collect and store vast amounts of sensitive personal information about their customers, making them attractive targets for cyberattacks. Regulatory standards require insurers to implement robust data security measures to protect this information from unauthorized access, use, or disclosure.

These measures may include encryption, firewalls, intrusion detection systems, and employee training programs. Insurers must also comply with privacy regulations, such as GDPR and CCPA, which govern how they collect, use, and share personal data.

Model Risk Management

Insurance companies rely heavily on models for pricing, reserving, and risk management. However, models are only as good as the data and assumptions that go into them. Model risk arises from the potential for errors or inaccuracies in these models, which can lead to poor decision-making and significant financial losses.

Regulatory standards increasingly require insurers to implement model risk management frameworks that address the entire model lifecycle, from development and validation to implementation and monitoring. These frameworks should include independent model validation, ongoing performance monitoring, and clear governance structures.

Challenges in Insurance Risk Management Regulatory Compliance

While regulatory compliance is essential, it also presents several challenges for insurers:

Complexity of Regulations

Insurance regulations can be complex and constantly evolving. Insurers must stay up-to-date on the latest regulatory requirements and adapt their risk management practices accordingly. This requires significant resources and expertise.

Data Availability and Quality

Effective risk management relies on accurate and reliable data. However, many insurers struggle with data availability and quality issues. This can make it difficult to accurately assess risks and make informed decisions.

Technology and Infrastructure

Implementing robust risk management systems requires significant investments in technology and infrastructure. Many insurers are using legacy systems that are not well-suited to modern risk management practices. Upgrading these systems can be costly and time-consuming.

Talent and Expertise

Effective risk management requires skilled professionals with expertise in actuarial science, finance, and risk management. However, there is a shortage of qualified professionals in these areas. Insurers must invest in training and development to build their risk management capabilities.

Global Consistency

For multinational insurers, complying with different regulatory standards across multiple jurisdictions can be challenging. Harmonizing risk management practices across different regions requires careful coordination and communication.

0 Comments