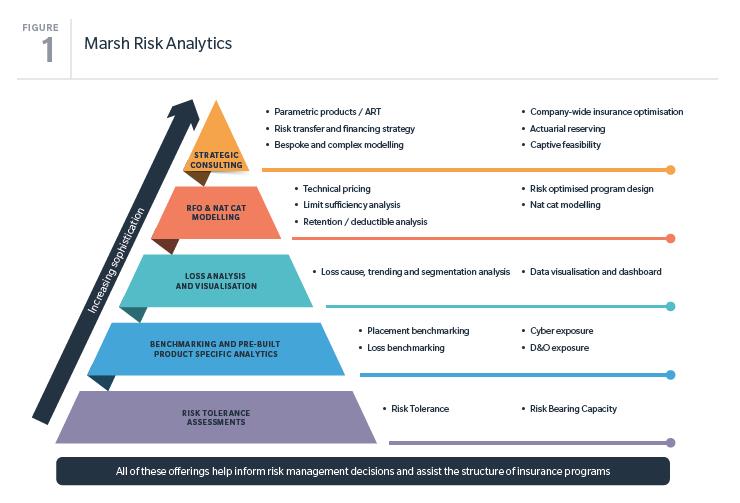

Understanding Real Estate Insurance Risk Management Assessment

Real estate investments, whether residential or commercial, represent significant financial commitments. Protecting these investments from potential risks is crucial for long-term financial security and success. A key component of this protection is a comprehensive real estate insurance risk management assessment. This assessment helps identify potential hazards, evaluate their potential impact, and develop strategies to mitigate those risks through appropriate insurance coverage and other risk management techniques.

The Importance of a Risk Management Assessment

A real estate insurance risk management assessment goes beyond simply purchasing a basic insurance policy. It involves a thorough analysis of the property, its location, and various external factors that could lead to financial loss. By understanding these risks, property owners can make informed decisions about the type and amount of insurance coverage needed, as well as implement preventative measures to reduce the likelihood of damage or loss.

Identifying Potential Risks

The first step in a risk management assessment is to identify potential hazards that could affect the property. These risks can be broadly categorized into several areas:

- Natural Disasters: This includes risks such as earthquakes, floods, hurricanes, tornadoes, wildfires, and other weather-related events. The location of the property significantly influences the likelihood and severity of these risks.

- Property Damage: This encompasses risks like fire, water damage (from leaks or burst pipes), vandalism, and structural damage. The age and condition of the property, as well as the materials used in its construction, can affect its vulnerability to these types of damage.

- Liability Risks: This includes potential lawsuits arising from injuries or accidents that occur on the property. For example, a slip and fall on a poorly maintained walkway or a dog bite incident.

- Financial Risks: This can include risks such as loss of rental income due to property damage or vacancy, as well as fluctuations in property value.

- Crime and Vandalism: Properties in high-crime areas are more susceptible to vandalism, theft, and other criminal activities. Security measures, such as alarm systems and security cameras, can help mitigate these risks.

The Assessment Process: A Step-by-Step Guide

Conducting a thorough real estate insurance risk management assessment involves several key steps:

1. Property Inspection

A detailed inspection of the property is essential to identify potential hazards and vulnerabilities. This inspection should include:

- Structural Assessment: Evaluating the foundation, roof, walls, and other structural components for signs of damage or deterioration.

- Electrical and Plumbing Systems: Checking the electrical wiring, plumbing pipes, and other systems for potential hazards, such as faulty wiring or leaky pipes.

- Hazard Identification: Identifying potential hazards such as asbestos, lead paint, or mold.

- Security Assessment: Evaluating the security measures in place, such as locks, alarms, and security cameras.

2. Location Analysis

The location of the property plays a significant role in its risk profile. A location analysis should consider:

- Natural Disaster Risks: Assessing the likelihood of natural disasters based on the property's geographic location. This can involve reviewing historical data and consulting with experts.

- Crime Rates: Evaluating the crime rates in the area to assess the risk of vandalism, theft, and other criminal activities.

- Environmental Factors: Considering environmental factors such as proximity to floodplains, fault lines, or industrial sites.

3. Insurance Policy Review

A thorough review of existing insurance policies is crucial to identify any gaps in coverage. This review should consider:

- Coverage Limits: Ensuring that the coverage limits are adequate to cover the full replacement cost of the property.

- Deductibles: Understanding the deductibles and how they will affect out-of-pocket expenses in the event of a claim.

- Exclusions: Identifying any exclusions in the policy that could limit coverage for specific types of damage or loss.

- Policy Type: Determining if the current policy type (e.g., homeowners, commercial property) is appropriate for the property and its use.

4. Risk Mitigation Strategies

Based on the findings of the assessment, develop strategies to mitigate the identified risks. This may involve:

- Improving Property Security: Installing alarm systems, security cameras, and other security measures.

- Making Property Improvements: Repairing structural damage, upgrading electrical and plumbing systems, and addressing other potential hazards.

- Implementing Preventative Maintenance: Regularly inspecting and maintaining the property to prevent damage and identify potential problems early on.

- Adjusting Insurance Coverage: Increasing coverage limits, adding endorsements for specific risks, or switching to a different type of policy.

5. Regular Updates and Reviews

A real estate insurance risk management assessment is not a one-time event. It should be regularly updated and reviewed to reflect changes in the property, its location, and the insurance market. This includes:

- Annual Policy Review: Reviewing insurance policies annually to ensure that they are still adequate and appropriate.

- Post-Event Assessment: Conducting a new assessment after any significant event, such as a natural disaster or major property damage.

- Market Updates: Staying informed about changes in the insurance market and adjusting coverage accordingly.

The Role of Professionals

While property owners can conduct a basic risk management assessment on their own, it is often beneficial to consult with professionals, such as:

Insurance Brokers

Insurance brokers can provide expert advice on the types and amounts of coverage needed, as well as help compare policies from different insurance companies. They can also assist with the claims process in the event of a loss.

Property Inspectors

Property inspectors can conduct thorough inspections of the property to identify potential hazards and vulnerabilities. They can provide detailed reports that can be used to develop risk mitigation strategies.

Risk Management Consultants

Risk management consultants specialize in identifying and assessing risks and developing strategies to mitigate those risks. They can provide comprehensive assessments and tailored recommendations for real estate investors.

Benefits of a Proactive Approach

Investing in a real estate insurance risk management assessment provides numerous benefits, including:

- Reduced Financial Losses: By identifying and mitigating potential risks, property owners can reduce the likelihood of financial losses due to property damage, liability claims, or other events.

- Peace of Mind: Knowing that the property is adequately protected can provide peace of mind and reduce stress.

- Improved Property Value: Implementing preventative maintenance and making property improvements can increase the value of the property.

- Lower Insurance Premiums: By demonstrating a commitment to risk management, property owners may be able to negotiate lower insurance premiums.

- Compliance with Regulations: In some cases, a risk management assessment may be required to comply with local regulations or lender requirements.

In conclusion, a comprehensive real estate insurance risk management assessment is an essential tool for protecting real estate investments. By identifying potential hazards, evaluating their impact, and implementing mitigation strategies, property owners can minimize their financial risks and ensure the long-term success of their investments. Taking a proactive approach to risk management is a smart investment that can pay off in the long run.

0 Comments