What is Non Owned Auto Insurance?

Non-owned auto insurance provides liability coverage when you drive a car you don't own. This typically includes rental cars, borrowed vehicles, or company cars used for personal reasons. It’s important to understand that non-owned auto insurance doesn't cover damage to the vehicle you're driving; it primarily covers bodily injury and property damage you cause to others in an accident.

Who Needs Non Owned Auto Insurance?

Several situations make non-owned auto insurance a worthwhile consideration:

- Frequent Renters: If you frequently rent cars, especially for extended periods, non-owned auto insurance can be more cost-effective than repeatedly purchasing coverage from the rental agency.

- Borrowers: If you often borrow cars from friends or family, non-owned auto insurance provides a layer of protection beyond the vehicle owner's policy.

- Employees Driving Company Cars: If you use a company car for personal errands or outside of work-related duties, your employer's insurance may not fully cover you. Non-owned auto insurance can fill this gap.

- Individuals Without a Personal Vehicle: Even if you don't own a car, you might occasionally need to drive. Non-owned auto insurance ensures you're protected in those instances.

- Those Seeking Additional Liability Coverage: If you want higher liability limits than your existing auto insurance policy provides, a non-owned policy can act as an umbrella policy, offering extra protection.

How Does Non Owned Auto Insurance Work?

Non-owned auto insurance acts as secondary coverage. This means that in the event of an accident, the vehicle owner's insurance policy will typically pay out first. However, if their coverage limits aren't sufficient to cover all the damages and injuries, your non-owned policy will kick in to cover the remaining costs, up to your policy's limits.

Think of it as a safety net that protects you from significant financial losses if you're at fault in an accident while driving a non-owned vehicle.

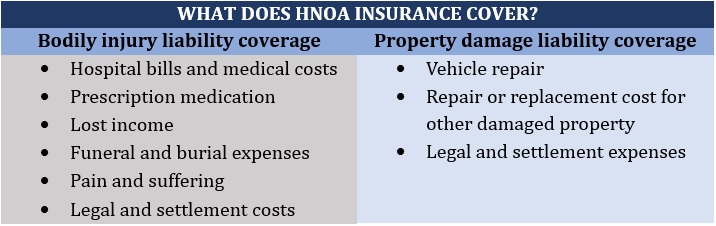

What Does Non Owned Auto Insurance Cover?

Non-owned auto insurance primarily covers:

- Bodily Injury Liability: This covers medical expenses, lost wages, and other costs associated with injuries you cause to another person in an accident.

- Property Damage Liability: This covers the cost of repairing or replacing property you damage in an accident, such as another vehicle, a fence, or a building.

- Legal Defense Costs: If you are sued as a result of an accident, non-owned auto insurance can cover your legal defense costs, regardless of whether you are ultimately found liable.

What Does Non Owned Auto Insurance NOT Cover?

It's equally important to understand what non-owned auto insurance doesn't cover:

- Damage to the Vehicle You're Driving: Non-owned auto insurance doesn't cover damage to the rental car, borrowed car, or company car you're driving. For that, you would need to rely on the vehicle owner's collision coverage or purchase supplemental coverage from the rental agency.

- Your Own Injuries: Non-owned auto insurance typically doesn't cover your own medical expenses or injuries sustained in an accident. You'll likely need to rely on your health insurance or personal injury protection (PIP) coverage (if applicable) for that.

- Vehicles You Own or Regularly Use: This type of insurance isn't meant to cover vehicles you own or vehicles you use frequently. It's specifically for occasional use of non-owned vehicles.

- Intentional Acts: Damages or injuries resulting from intentional acts are not covered.

- Business Use in Some Cases: Certain policies may exclude coverage for business use, especially if you're using the vehicle for commercial purposes.

How Much Does Non Owned Auto Insurance Cost?

The cost of non-owned auto insurance varies depending on several factors, including:

- Your Driving Record: A clean driving record will typically result in lower premiums.

- Your Location: Insurance rates vary by state and even by ZIP code.

- Coverage Limits: Higher liability limits will generally result in higher premiums.

- Insurance Company: Different insurance companies offer different rates.

Generally, non-owned auto insurance is less expensive than a standard auto insurance policy because it only provides liability coverage and doesn't cover damage to the vehicle you're driving. To get an accurate estimate, it’s best to get quotes from several different insurance providers.

How to Get Non Owned Auto Insurance

Getting non-owned auto insurance is usually a straightforward process:

- Shop Around: Compare quotes from multiple insurance companies to find the best rates and coverage options. Many online tools allow you to get quotes quickly.

- Provide Information: You'll need to provide information about your driving history, address, and desired coverage limits.

- Review the Policy: Carefully review the policy terms and conditions to understand what is covered and what is not.

- Purchase the Policy: Once you're satisfied with the coverage and price, you can purchase the policy.

Non Owned Auto Insurance vs. Standard Auto Insurance

Key Differences

While both types of insurance offer liability protection, there are key differences:

- Vehicle Ownership: Standard auto insurance covers vehicles you own, while non-owned auto insurance covers vehicles you don't own.

- Coverage Scope: Standard auto insurance can include collision, comprehensive, and other coverages in addition to liability, while non-owned auto insurance typically only provides liability coverage.

- Primary vs. Secondary: Standard auto insurance is primary coverage for your own vehicle, while non-owned auto insurance is secondary coverage when driving someone else's vehicle.

When is Non Owned Auto Insurance a Good Idea?

Here are some scenarios where non-owned auto insurance can be particularly beneficial:

- You frequently rent cars but don't want to purchase rental car insurance every time.

- You often borrow a friend's or family member's car and want to ensure you have adequate liability coverage.

- You use a company car for personal use and your employer's insurance policy doesn't fully cover you.

- You don't own a car but occasionally drive and want to be protected in case of an accident.

- You want to supplement your existing auto insurance policy with higher liability limits.

Understanding the Limits of Your Coverage

It is crucial to understand the limits of your non-owned auto insurance policy. The policy will specify the maximum amount it will pay for bodily injury liability and property damage liability. Ensure these limits are sufficient to protect you from potential financial losses in a serious accident. Consider your assets and potential exposure when choosing your coverage limits.

Read the Fine Print

As with any insurance policy, it's essential to read the fine print of your non-owned auto insurance policy. Pay attention to any exclusions, limitations, or special conditions that may apply. If you have any questions, don't hesitate to contact your insurance provider for clarification.

Conclusion

While this article provides a comprehensive overview of non-owned auto insurance, it is not a substitute for professional advice. Consult with an insurance agent or broker to determine if non-owned auto insurance is right for your specific situation and to ensure you have adequate coverage. They can help you assess your risk factors, compare quotes from different insurance companies, and choose a policy that meets your needs and budget.

0 Comments